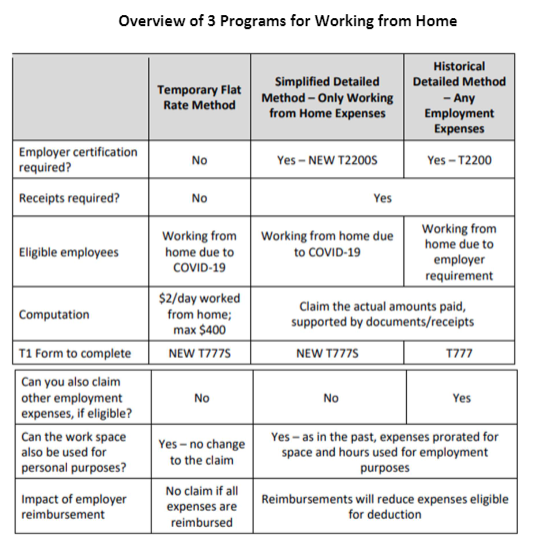

Temporary Flat Rate (TFR) Method - for employees who claim a flat amount ($2/day to a maximum of $400). No employer certification or supporting documentation for expenses will be required.

To claim the TFR, the employee must meet all the conditions below:

- the employee worked from home in 2020 due to the COVID-19pandemic;

- the employee worked more than 50% of the time from home for a period of at least four consecutive weeks in 2020;

- the employee is not claiming any other employment expenses; and

- the employer did not reimbursed all of the employee’s home office expenses. If the employer reimbursed some of the home office expenses, they could still make a claim.

Full time and Part Time employees qualify if the 50% condition is met.

CRA has also stated that if multiple people working from the same home each meet the above eligibility criteria; each can make a full TFR claim.

Detailed Method – Only Working from Home Expenses

- Simplified – for employees who claim actual expenses related to working from home, supported by receipts. Employer certification will be required.

As an alternative to the temporary flat rate method, eligible employees can also choose to use the detailed method to claim amounts paid for the period that the employee worked from home. This method requires the same calculation as a traditional workspace in the home claim but allows for the use of a simplified T2200S and T777S.

To use the detailed method, all the below conditions must be met:

- the employee worked from home in 2020 due to the COVID-19 pandemic (as in the past, a claim is also available if the employer required the employee to work from home);

- the employee was required to pay for expenses related to the workspace in theirhome;

- the employee worked more than 50% of the time from home for a period of at least four consecutive weeks in 2020 (as in the past, the deduction may also be available if the workspace was used exclusively for employment, and to meet clients, customers, or other people on a regular and continuous basis in the course of their employment);

- the employee has a completed and signed Form T2200S from their employer (or, as in the past, a Form T2200 certifying that they were required to work from home); and

- the expenses were used directly in the work during the period.

New short form T2200S

This form asks three questions:

- Did this employee work from home due to COVID-19?

- Did you or will you reimburse this employee for any of their home office expenses?

- Was the amount included on this employee's T4 slip?

The amount of any reimbursement or allowance is not required to be included on T2200S. but they cannot have reimbursed ALL of the expenses or the employee becomes ineligible for the claim.

CRA will accept an electronic signature on Form T2200S and Form T2200 for 2020. They are trying to legislate that this is acceptable going forward but currently it is just for 2020.